For many UK homeowners, leasehold property can feel unnecessarily complex. Terms such as lease extension and lease renewal are often used interchangeably, even though they refer to very different legal processes. Understanding the difference between the two is essential if you want to protect the value of your property, plan ahead, and avoid unexpected costs.

This guide explains what lease extension and lease renewal mean in the UK, how they differ, and when each option may apply to you as a leaseholder.

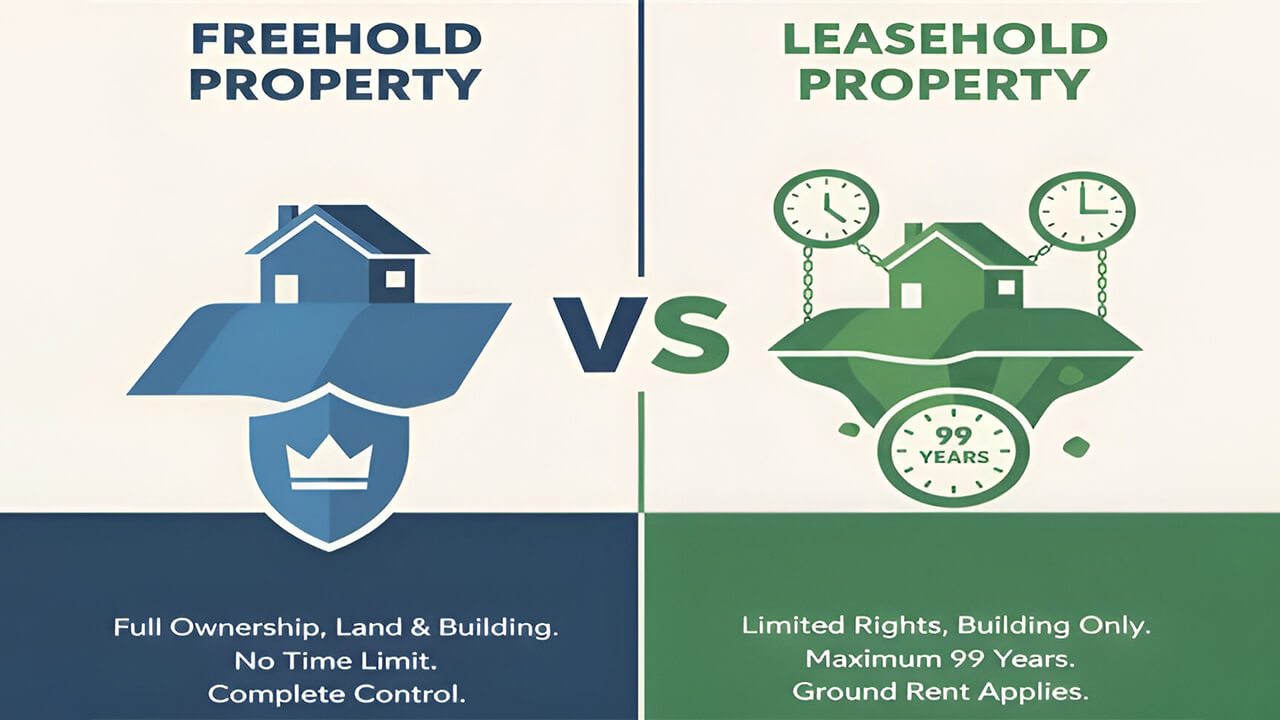

1. Understanding Leasehold Ownership in the UK

In a leasehold arrangement, you own the property for a fixed period of time, but not the land it stands on. The land remains owned by the freeholder. When the lease expires, ownership technically reverts to the freeholder unless action is taken.

Many residential leases start at 99 or 125 years, which can feel like a long time. However, once the lease term drops below certain thresholds, particularly 80 years, the property can lose value and become harder to sell or remortgage. This is why lease extension or renewal becomes an important consideration.

2. What Is a Lease Extension?

A lease extension is the legal process of increasing the remaining length of an existing lease. For most flat owners in England and Wales, this is a statutory right under the Leasehold Reform, Housing and Urban Development Act 1993.

Under this process, qualifying leaseholders are entitled to add 90 years to their existing lease term. Importantly, ground rent is reduced to a nominal amount, often referred to as a “peppercorn”.

Lease extensions are commonly used by residential leaseholders who want to secure the long-term value of their home and remove the risks associated with a short lease.

3. Why Lease Extensions Matter for Homeowners

As a lease shortens, the property typically becomes less attractive to buyers and lenders. Mortgage providers often refuse to lend on properties with short leases, which limits the pool of potential buyers.

Extending a lease can help to stabilise and even increase property value. It also provides peace of mind, as the extended term can last well beyond the leaseholder’s lifetime.

Another key factor is cost. Once a lease falls below 80 years, additional costs known as marriage value are usually payable. This makes early action financially sensible for many leaseholders.

Also read more about: How to Calculate a Lease Extension Valuation?

4. What Is a Lease Renewal?

A lease renewal involves replacing an existing lease with a new one, usually through negotiation with the freeholder. Unlike lease extensions, lease renewals are not always governed by statutory rights, particularly in residential cases.

Lease renewals are more common in commercial property or in situations where a leaseholder does not qualify for a statutory lease extension. The terms of the new lease, including length, rent, and conditions, are negotiated rather than fixed by legislation.

Because of this flexibility, renewals can vary significantly and may not always be favourable to the leaseholder without careful advice and valuation.

5. Key Differences Between Lease Extension and Lease Renewal

Although both processes deal with extending occupancy rights, their legal basis and outcomes are very different.

A lease extension follows a structured legal framework, offering protection and predictable outcomes for qualifying leaseholders. A lease renewal, by contrast, relies on negotiation and agreement, which means terms can vary widely.

Lease extensions usually remove ground rent, while renewals may include revised or even increased rent terms. Leaseholders pursuing a renewal need to carefully assess whether the new lease genuinely improves their position.

6. Cost Implications to Consider

Both lease extensions and lease renewals involve costs, but how those costs are calculated differs.

In a lease extension, the premium payable to the freeholder is calculated using established valuation principles. These take into account factors such as remaining lease length, property value, and future income loss to the freeholder.

In a lease renewal, costs are less predictable. The freeholder may request higher payments, ongoing rent, or additional clauses. Without accurate valuation input, leaseholders risk agreeing to unfavourable terms.

This is why professional leasehold valuation plays a crucial role in both scenarios.

7. Legal Process and Timeframes

A statutory lease extension follows a defined legal route. It begins with serving a formal notice, followed by negotiation and, if necessary, tribunal determination. While structured, the process can take several months to complete.

Lease renewals do not follow a fixed timeline. Some renewals are agreed quickly, while others can become prolonged if negotiations stall or disagreements arise.

Understanding the expected timescale helps leaseholders plan, especially if selling or refinancing the property is a priority.

8. The Role of Professional Valuation

Valuation is at the heart of both lease extension and lease renewal decisions. An accurate assessment helps leaseholders understand what is fair, what is negotiable, and what could become costly in the long run.

Professional valuation supports informed decision-making by clarifying the financial impact of different options. It also strengthens the leaseholder’s position when dealing with freeholders or legal representatives.

For many leaseholders, having clear valuation insight removes uncertainty and reduces the risk of overpaying.

9. Making the Right Choice as a Leaseholder

Choosing between a lease extension and a lease renewal depends on your property type, lease length, and legal eligibility. Residential leaseholders with statutory rights often benefit most from a lease extension, while renewals may be relevant in commercial or non-qualifying cases.

The most important step is understanding your position early and seeking reliable professional guidance before costs escalate or options become limited.

Final Thoughts

Lease extension and lease renewal may sound similar, but they serve different purposes and carry different risks and benefits. Knowing the distinction allows leaseholders to act confidently and protect their long-term interests.

For UK leaseholders navigating these decisions, informed valuation insight is a crucial foundation. Exploring specialist leasehold valuation services, such as those provided by Leasehold Valuations, can help ensure that choices around extending or renewing a lease are based on clarity, fairness, and long-term value rather than uncertainty.